Before you file: The Tax Changes for Upcoming Tax Season

Disclaimer: As an Amazon Associate I may earn from qualifying purchases from products mentioned on posts made on this site.

The start of the new year brings the focus back to preparing for one of the busiest and most dreaded times of the year for business owners and employees alike: tax season.

If you made any sort of income in 2020 – which you hopefully did – you will need to file your annual tax return, and you will want to start preparing as soon as possible so you are not caught by surprise in April.

And although there are not too many huge changes for the 2021 tax season, you will want to be made aware of what these changes are before you start on your paperwork. Fortunately, there is a lot of good news on this list. Read on to find out more.

Standard Deductions

To begin with, the 2021 tax season comes with higher standard deductions for both individuals and those filing jointly. There has been a $150 increase across all filing statuses, although if you are married filing jointly, you will receive a $300 increase. There are also small increases for those who are 65 and older or are blind. And if you are both 65 or older and blind, you will receive double the amount.

Popular Tax Credits

Tax credits are more valuable than deductions, as they directly reduce the amount of taxes you will owe. Some of the popular tax credits include the earned income tax credit, the child tax credit, the saver’s credit, and two educational tax credits. Income amounts have increased slightly for the earned income tax credit.

For the saver’s tax credit, you can earn up to $1,000 per person for money that has been contributed to retirement funds. Depending on your income level, you can earn credit on up to 50% of your contributions.

Finally, the Lifetime Learning tax credit offers tax breaks on educational expenses beyond bachelor’s degrees. If you make less than $59,000 a year, you can get a 20% tax credit on up to $10,000 in eligible expenses that have gone toward graduate school, vocational training, or other non-traditional education. This is an increase of $1,000 from last year.

Retirement Accounts

Retirement accounts are great to have because they get tax-deferred, but you can still get upfront tax deductions. Although IRA and 401k contribution limits remain the same as last year, the income limits for both are changing slightly.

This is important because if your income level falls above the cutoff, you will not be eligible for a deduction. Since it has been raised, more people will be eligible for a deduction.

Additionally, in previous years, the IRS has required mandatory withdrawals from retirement investment accounts when you reach the age of 72, which can then be taxed as income.

However, because of the CARES act and the stock market dip, you will not have to make these mandatory withdrawals and therefore won’t have to report that income on your 2021 tax returns as income.

Healthcare & Education

Some plans, such as 529 plans, allow you to set aside money for education in a separate account that can be tax-deferred. However, these must be used for qualifying educational expenses. There are no income limits for 529 plans. Additionally, if your employer helped to pay for your college tuition or school expenses in 2020, this payment will not be taxed up to a certain amount.

You can do a similar thing for healthcare. You can set money aside for healthcare expenses that are tax-free if you have high deductible health insurance. In 2021, the limit on the maximum amount of money that can be placed into this account will increase.

Gift & Estate Tax Exemptions

The estate tax lifetime exclusion is the amount of money you can pass on without paying taxes. In 2021, this will increase from $11.58 million to $11.7 million. The gift tax exclusion remains unchanged.

Charitable Giving

Because of the widespread struggle caused by COVID-19, the CARES act has made it easier to get a tax break for charitable giving, to encourage more people to donate to those in need. Typically, charitable giving can only be written off when you itemize your deductions, but in 2021 you will be able to write off up to $300 per person in donations even if you take the standard deduction.

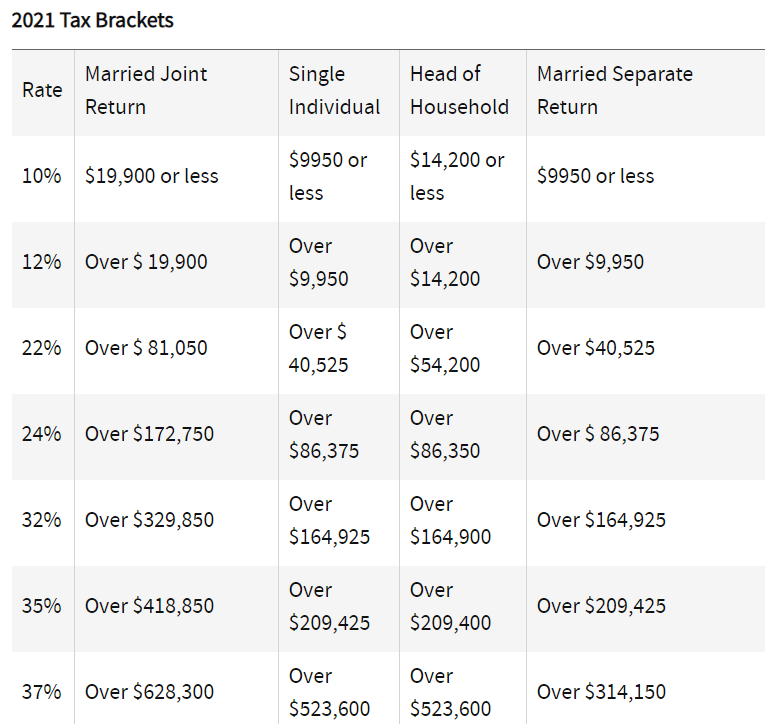

Tax Brackets

Tax brackets are used to determine the rate at which everyone is taxed. They differ for those who file as single, married filing jointly, and head of household. Typically, the more income you earn, the higher rate you are taxed at. 2021 spells good news for everyone, though, as tax brackets have increased by a few hundred dollars at every level around the board, for every filing status.

Conclusion

In conclusion, there are several changes to the way taxes are going to be filed in 2021. Even though these changes are minor, they may make a big impact on your family.

The good news is that most of these changes will likely make a positive impact, as they tend to include more savings, more tax breaks, and more people included in lower tax brackets, as well as an encouragement for further charitable giving and savings for everything from retirement, to education, to healthcare.

Notice: Amazon and the Amazon logo are trademarks of Amazon.com, Inc, or its affiliates.